Introduction

If you’re not sure about how much to put into your 401(k) you’re not alone. This quick guide shows you how to decide a savings rate you can stick with, why the employer match matters, and how Pocket Plan helps you set, test, and track your goal—no matter where you’re starting.

What is a 401(k)?

A 401(k) is an employer-sponsored retirement plan that lets you invest for the future with tax advantages. Plans differ by company, but the basics are the same: you contribute from your paycheck, your money grows tax-advantaged, and some employers add an employer match.

Note: This article gives general guidelines, not individualized advice.

Key Things to Consider (Before You Pick a Number)

- Employer Match: Many employers match part of what you contribute to your 401k. Aim to contribute at least enough to get the full match—it’s part of your compensation.

For instance, an employer may provide a 100% match up to 3% of your compensation. If you contribute 3% of your paycheck, your employer contributes another 3%. That gives you a 6% total contribution to your retirement.

- Taxes:

- Traditional (pre-tax) Contributions: Lowers today’s taxable income; you pay taxes in retirement.

- Roth (after-tax) Contributions: No deduction now; qualified withdrawals can be tax-free later.

- Traditional (pre-tax) Contributions: Lowers today’s taxable income; you pay taxes in retirement.

- Budget & Affordability: Start with what you can sustain. You can raise your rate over time.

- Compound Growth: Dollars invested earlier have more years to grow.

Pocket Plan Tip: In My Plan → Retirement Score, connect your 401(k) by adding an account. Pocket Plan will add the account value and investments to your plan to track activity and performance.

Step-by-Step: Figure Out Your 401(k) Savings Rate

- Capture Your Employer Match (Minimum Target).

- Find your plan’s match rule (e.g., “100% of the first 3%” or “50% of the first 6%”).

- Set your contribution to at least the level that earns the full match.

- Find your plan’s match rule (e.g., “100% of the first 3%” or “50% of the first 6%”).

- Pick an Initial Savings Target.

- A common starting point is 10–15% of gross pay, including employer match.

- If that’s too high today, start smaller (even 3–6%) and plan to increase.

- A common starting point is 10–15% of gross pay, including employer match.

- Stress-Test in Pocket Plan.

- Go to Scenarios → Savings Rate.

- Run a scenario at your current rate, then at +1% and +2% to see the impact on your Retirement Score and projected savings.

- Go to Scenarios → Savings Rate.

- Choose Traditional vs. Roth (or a mix).

- Use Scenarios → Tax Treatment to compare after-tax outcomes and the effect on take-home pay.

- Use Scenarios → Tax Treatment to compare after-tax outcomes and the effect on take-home pay.

- Set Auto-Increase.

- If your plan supports it, enable Auto-Increase (e.g., +1% every 6–12 months) until you reach your target.

- If your plan supports it, enable Auto-Increase (e.g., +1% every 6–12 months) until you reach your target.

- Align With Your Budget.

- In Cash Flow, confirm your contribution won’t jeopardize essentials.

- Use Paycheck Preview (if available) to see your new take-home pay.

- In Cash Flow, confirm your contribution won’t jeopardize essentials.

- Use Milestones to Bump Your Rate.

- Schedule a +1% increase with raises, bonuses, or debt payoffs.

- Schedule a +1% increase with raises, bonuses, or debt payoffs.

- If You’re 50+: Add Catch-Up Contributions.

- Many plans allow extra contributions after age 50.

- Toggle “Enable Catch-Up” in PocketPlan when eligible.

- Many plans allow extra contributions after age 50.

- Review Quarterly.

- Use your Pocket Plan Retirement Score to check progress. Adjust your rate or timeline as life changes.

- Use your Pocket Plan Retirement Score to check progress. Adjust your rate or timeline as life changes.

General Guidelines (Flexible, Not Rules)

- Aim for 10–15% of income (including match) across your working years.

- Can’t hit it now? Start where you are and step up regularly. Consistency matters more than perfection.

Age-Based Benchmarks (Helpful Waypoints)

- 20s: Start early—even modest contributions build the habit and harness compounding.

- 30s: Increase as income stabilizes; a common waypoint is ~1× salary saved by 30.

- 40s: Keep ramping; rough targets are ~3× salary by 40 and 6× by 50.

- 50s–60s: Leverage catch-up contributions; fine-tune retirement age and income needs.

These are averages—not judgments. If you’re behind, focus on the next step up.

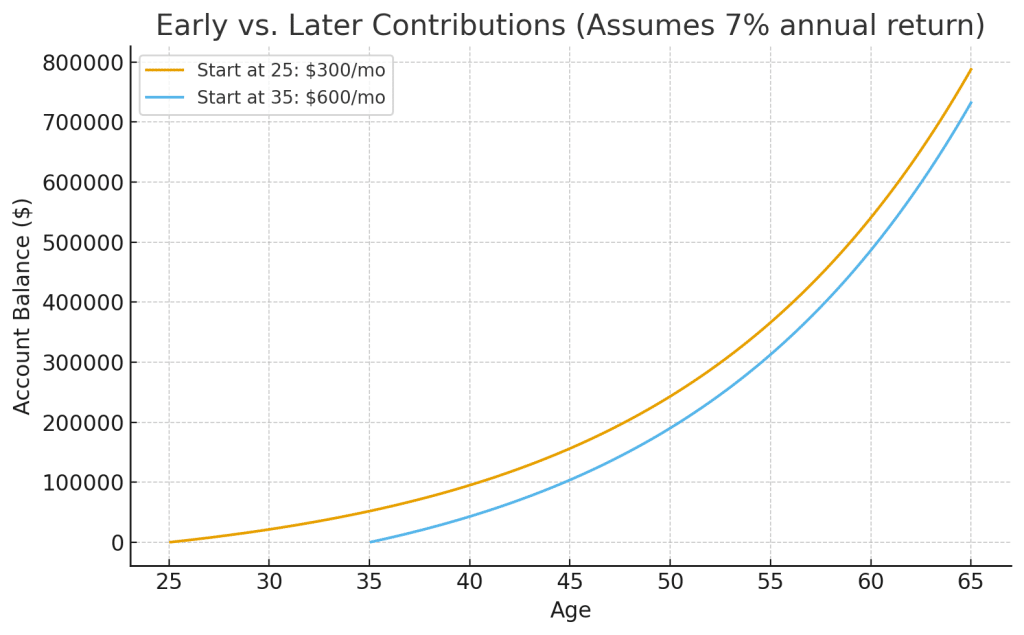

PocketPlan Visual: Early vs. Later Contributions

(Illustrative only—assumes steady returns; your results will vary.)

The chart above shows how smaller, earlier contributions can rival larger, later contributions thanks to compounding.

Other Factors to Keep in Mind

- Job or Income Changes: Update your contribution when salary changes.

- Leaving a Company: Understand rollover options to avoid taxes and penalties.

- Investment Mix: Contributions matter—and so does how you invest. Review your allocation in plan menus or with an advisor.

- Retirement Lifestyle: Savings needs depend on goals (location, spending, retirement age).

Precautions

- Avoid Early Withdrawals: They often trigger penalties and stunt long-term growth.

- Ask for Professional Advice: Use your plan’s advice tools or a fiduciary advisor for personalized guidance.

How to Get Started Today (PocketPlan Workflow)

- Connect your 401(k) (and employer details) in Accounts.

- Set your contribution to capture the full match.

- Run a Savings Rate Scenario (+1% and +2%) in Scenarios.

- Enable Auto-Increase until you reach your target.

- Check Retirement Score quarterly and adjust as needed.

Troubleshooting in PocketPlan

- No employer match showing? Refresh accounts; confirm plan details under Personal Info → Employment.

- Contribution not updating? Re-sync payroll provider or manually enter the new rate in Plan Settings.

- No Auto-Increase option? Some plans don’t support it—reach out to your HR provider or Financial Advisor to help review your options.

- Self-employed? Consider a Solo 401(k) or SEP IRA; model the contribution in Scenarios.

Conclusion

Small, steady increases—especially started early—add up. Use PocketPlan’s Retirement Score, Scenarios, and Auto-Increase to set a realistic 401(k) savings rate and keep improving it over time.

Next Steps

- Explore: Scenarios → Savings Rate

- Learn more: Traditional vs. Roth in PocketPlan

- Related: How to Roll Over a 401(k)

—————————————————————————————————————————–

DO NOT POST CONTENT TO BLOG

Blog Outline: How Much Should You Save in Your 401(k)?

Introduction

– Short, welcoming hook that acknowledges the uncertainty many people feel around saving for retirement.

– Statement of purpose: This blog will walk through how much to save, key factors to consider, and how savings goals can vary by age and stage of life.

– Tone guidance: Neutral, reassuring, and optimistic. Emphasize that no matter where someone is starting from, progress is possible.

What is a 401(k)? (Context for All Readers)

– Simple definition of a 401(k) as a workplace retirement savings account.

– Note that plans may vary by employer, but all share the same basic foundation of tax advantages and potential growth.

– Emphasize that while this isn’t individual financial advice, these are useful general guidelines.

Key Considerations Before Deciding How Much to Save

– Employer Match: Explain how an employer match works and why it’s important to contribute at least enough to get the full match.

– Tax Advantages: Distinguish between pre-tax (traditional) and after-tax (Roth) contributions in plain language.

– Budget & Affordability: Encourage readers to contribute what they can without jeopardizing essentials; note that contributions can often start small and grow over time.

– Compound Growth: Brief explanation of how early contributions can accumulate over decades.

Visual: A simple chart showing “small early contributions growing significantly over time” vs. “larger later contributions.” Keep it approachable and non-intimidating.

General Contribution Guidelines

– Start with broad, commonly cited targets:

– Rule of thumb: Save between 10–15% of income, including employer match.

– Stress flexibility: “If that’s not realistic for you today, even starting smaller builds a strong habit.”

– Highlight that these are guidelines, not hard rules, and personal circumstances matter.

Age-Based Benchmarks

– In Your 20s: Focus on starting early, even with modest contributions. Habit and time are advantages.

– In Your 30s: Aim to increase contributions as income stabilizes. Consider aiming to have about 1x annual salary saved by age 30.

– In Your 40s: Contributions should ideally ramp up; goal is roughly 3x salary by 40, 6x by 50.

– In Your 50s & 60s: Catch-up contributions become important; retirement planning horizon grows shorter.

– Emphasize that these benchmarks are averages and not judgments. Start where you are.

Visual: A timeline or ladder graphic showing approximate “ratios of salary saved by decade” (e.g., 1x at 30, 3x at 40, 6x at 50, etc.), using a friendly infographic style.

Other Important Factors

– Job and Income Changes: Adjusting contributions when salary grows or when switching employers.

– Portability of 401(k): Understanding rollovers if leaving a company.

– Diversification & Investment Choices: Very brief high-level note that contributions aren’t everything—investment selection also plays a role.

– Retirement horizon and lifestyle considerations: Not all retirement goals look the same; savings needs depend on individual expectations.

Precautionary Notes

– Stress the importance of avoiding early withdrawals, due to penalties and reduced long-term growth.

– Mention the value of professional advice for individual situations, reinforcing trustworthiness.

How to Get Started Today

– Encourage readers to review their current contribution percentage.

– Suggest starting by capturing the employer match, then gradually increasing contributions over time.

– Offer positive reassurance that “it’s never too early and never too late” to improve saving habits.

Conclusion

– Reiterate the key takeaway: small, consistent contributions have a big impact over time.

– Encourage readers to see their 401(k) savings as a way to feel more secure about their financial future.

– Invite readers to check resources (your fintech platform’s features or tools) for calculators, guidance, or account management.

Visual: An uplifting image of a confident, diverse group of people looking toward the future (symbolic, not niche-specific). Caption: “Building security for the future—step by step.”

——————————————————————————————————————————-